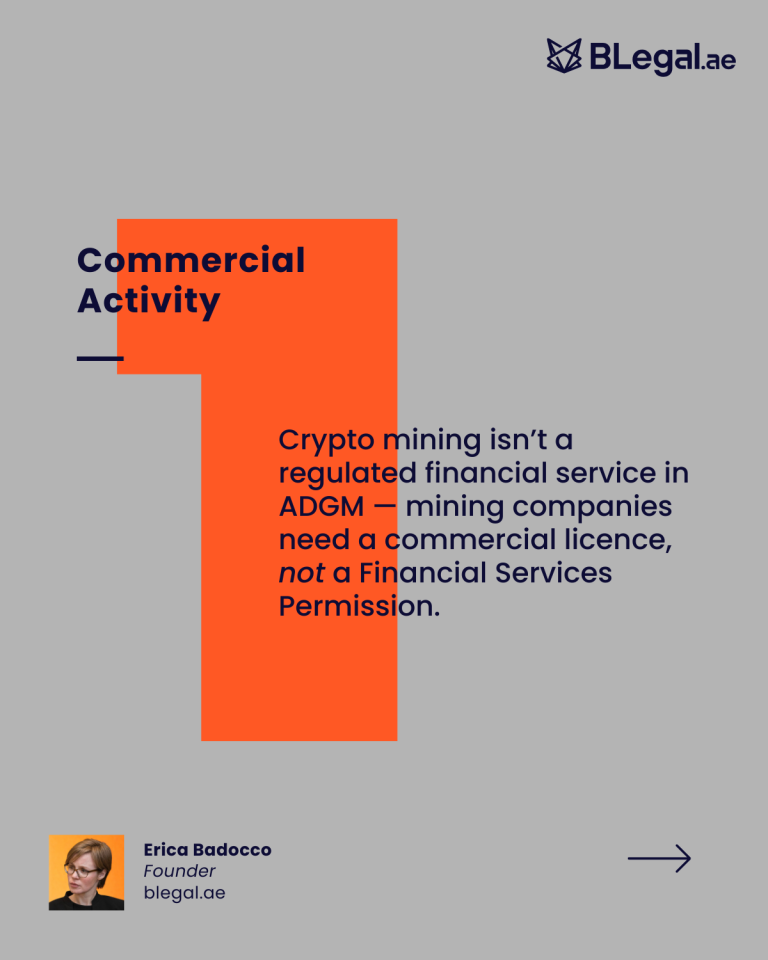

In most cases, if you are simply mining BTC or other layer 1 tokens, you would not typically be considered a token issuer in ADGM. That distinction is important because mining a protocol-native asset is usually very different from issuing a project token that represents rights, claims, or exposure to an underlying asset.

Mining rewards generally do not trigger the same token issuance implications that may arise with project tokens, including tokens linked to RWAs, funds, bonds, or equity structures.

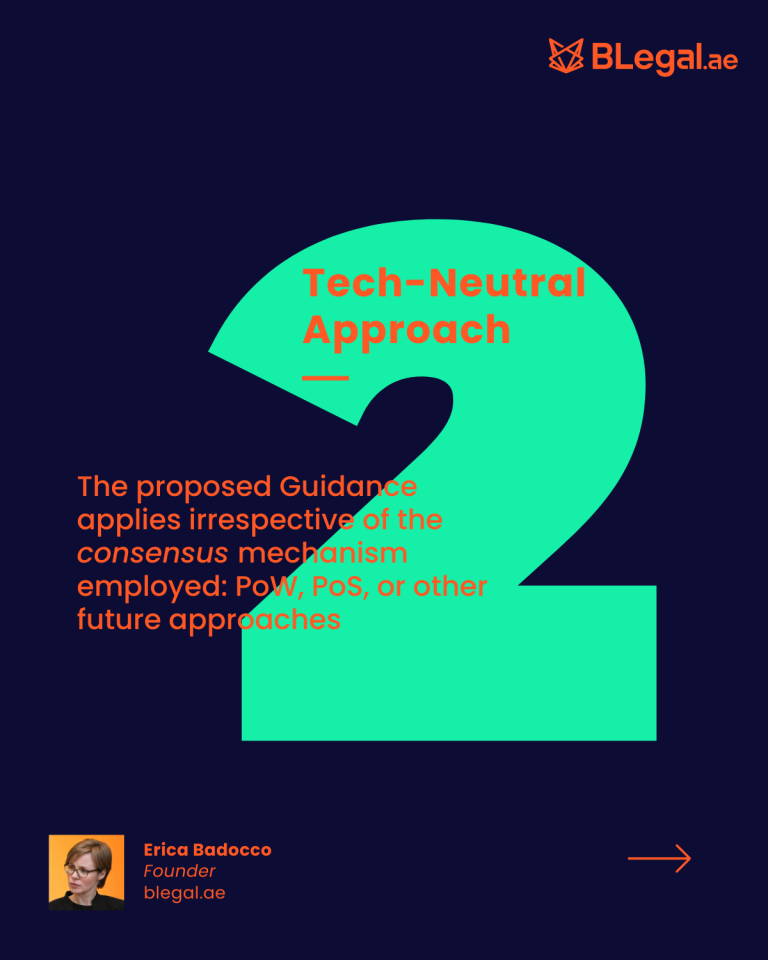

1. Mining usually produces a protocol-native asset

With Bitcoin mining, there is generally no separate issuer creating and offering a token to the public. The asset is generated through the operation of the network protocol.

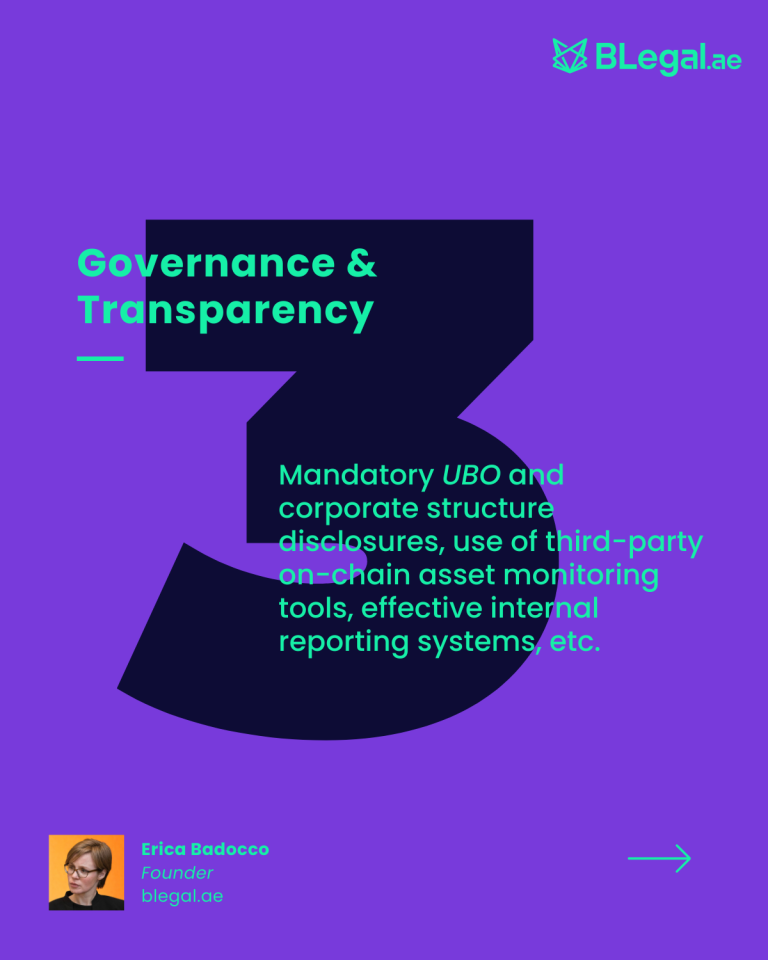

2. Project tokens may involve issuance considerations

By contrast, project tokens are often created and distributed by an identifiable issuer. Where those tokens represent rights, claims, or economic interests, they may trigger digital asset and/or financial services considerations depending on structure and jurisdiction.

3. Regulatory analysis depends on the facts

Even where an activity appears straightforward, the legal treatment can depend on how the activity is structured, marketed, and carried out in practice.

ADGM consultation on crypto mining

ADGM has recently opened a consultation on proposed guidance for crypto mining activities. This is a useful development for businesses assessing how mining-related activity may be viewed in Abu Dhabi Global Market.

Below are the main points from our carousel summary.